Visa and Mastercard payments are convenient for customers, but can cost merchants high processing fees. Atoa Payments wants to provide a cheaper alternative that is still easy for customers to use. The London-based fintech announced today that it has raised $2.2 million in pre-seed funding.

The round was led by Leo Capital and Passion Capital, with participation from angel investors like GoCardless and Nested co-founder Matt Robinson, Moon Capital Ventures and MarketFinance co-founder Anil Stocker.

Atoa co-founder Sid Narayanan told TechCrunch that he and co-founder Cian O’Dowd developed the idea for Atoa after selling their previous startup, expense management platform KlearCard, to Singapore fintech Validus in 2021.

Their barber, who initially accepted card payments, started asking for cash payments or bank transfers because he wanted to reduce his card processing fees, which were around 1.6%. Narayanan and O’Dowd were used to card alternative payments after living in Singapore, and saw an opportunity to use the U.K.’s open banking payments stack to build a Visa and Mastercard alternative, Narayanan told TechCrunch.

Mastercard and Visa payment rails can cost small merchants and their customers net margins of 51%, with card machine fees of about 1.75%, Narayanan said. Atoa, on the other hand, charges a fixed percentage fee billable to merchant each months that is up to 70% lower than debit cards. It also does not have hardware rentals, service fees or PCI attestation of compliance charges.

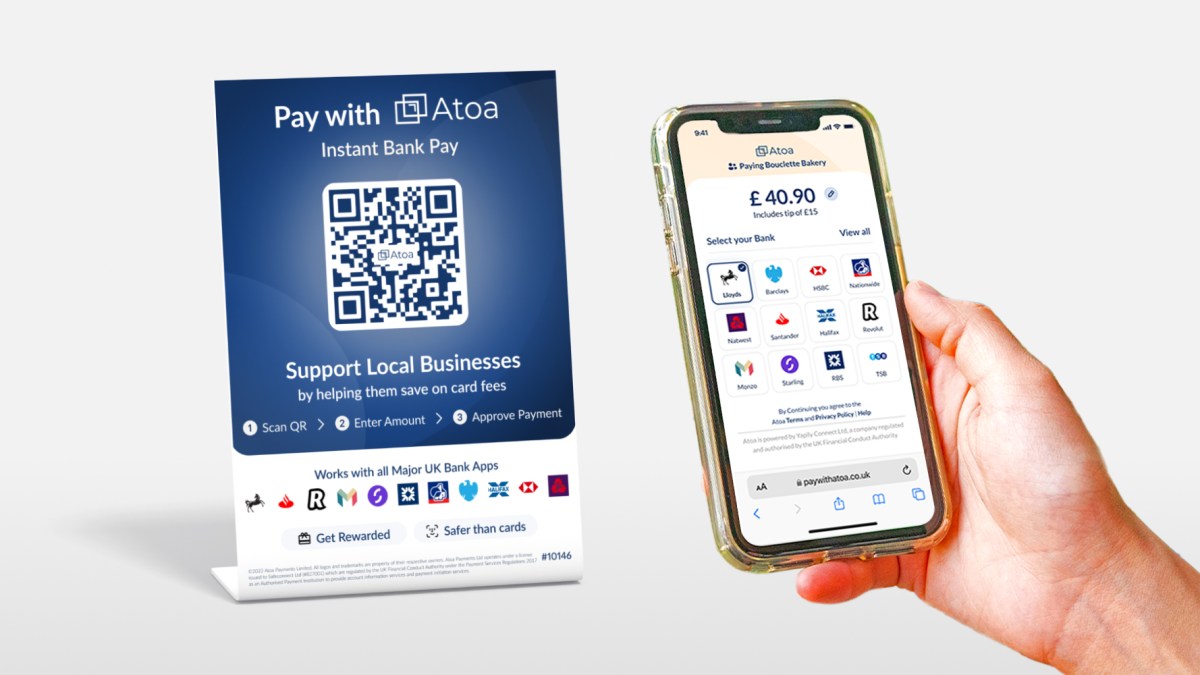

To use Atoa, merchants download an app that connects to their bank accounts. Customers don’t need to download Atoa’s app to use the service. Instead, they can use Atoa as long as they have a U.K. mobile banking app. According to Narayanan, the majority of adults, or about 80% in the U.K., already have a mobile banking app on their phone, removing the main source of friction. Merchants send a link for payment by SMS, PayBay or offer a QR code to scan.

To incentivize more customers to use Atoa, the startup also plans to add rewards and loyalty benefits, like digital scratch cards that can let them get cash rewards into their existing U.K. bank accounts.

Once customers pay with Atoa, merchants to receive payment instantly through Instant Bank Pay. They also get funds in their bank account right away, instead of waiting for up to 1 to 2 business days.

Atoa says since it went live in June, it’s gotten more than 100% month-on-month total payment volume (TPV) growth and merchant customers. Its most direct competitors include card machine providers like SumUp, Zettle, Square and Barclaycard, Narayanan said. Atoa differentiates by offering lower fees and enabling merchants to receive funds more quickly than the three days typically required by card machine providers. It also charges lower fees than players that are intermediated by Visa and Mastercard.

In a statement about its investment, Passion Capital partner Robert Dighero said, “Atoa has come to the UK market at the right time to leverage open banking and bring to small and medium sized merchants a truly viable alternative to payment cards and card machines that can be deployed in-store within minutes. We’re delighted to work with the Atoa team after their first fintech success and look forward to partnering with them as they achieve even greater heights with Atoa.”

Comments are closed, but trackbacks and pingbacks are open.