[ad_1]

Who has the best mortgage rates?

We analyzed data from the 40 biggest lenders in the U.S., looking for the lowest interest rates and fees.1,2 These lenders topped the list for best 30–year mortgage rates:

(1) Freedom Mortgage, (2) Better Mortgage, (3) Citibank, (4) Guild Mortgage Company, (5) American Financial Network.

Remember that rates vary a lot from person to person, so there’s a good chance your best rate will come from a company not listed above. Be sure to shop for your best offer.

Get started mortgage rate shopping (Feb 21st, 2022)

In this article (Skip to…)

Today’s best mortgage rates

Not only can mortgage rates change on a daily basis, they often adjust multiple times per day. If you’re in the market for a home loan, you’ll want to keep an eye on those movements.

Knowing when rates are rising or falling can help you decide when to lock a rate – especially if you’re refinancing. And it can give you some idea of how competitive your own rates are compared to the overall market.

To give you a basis for comparison, here are today’s best mortgage rates according to our lender network.*

| Loan Type | Today’s Best Mortgage Rate* |

| Conventional 30-Year Fixed | % (% APR) |

| Conventional 15-Year Fixed | % (% APR) |

| FHA 30-Year Fixed | % (% APR) |

| FHA 15-Year Fixed | % (% APR) |

| VA 30-Year Fixed | % (% APR) |

| VA 15-Year Fixed | % (% APR) |

*Rates shown here are based on a daily survey of The Mortgage Reports’ lender network. Your own rate will be different. See our full mortgage rate assumption here.

How to find your lowest mortgage rate

Mortgage rates are highly personal. Factors like your credit score and debt–to–income ratio (DTI) will have a big impact on the rate you get.

That means the company with the lowest average rates won’t always be the cheapest lender for everyone.

For example: Among the 40 mortgage lenders in our study, Freedom Mortgage had the lowest average mortgage rate in 2020, at just 2.92% for a 30–year loan.

But average rates tell only part of the story. Overall, Freedom Mortgage rates ranged from under 2% to over 6%. So some people got much lower rates than others.

To find your best mortgage lender, you have to request rate quotes from more than one company and compare offers.

Compare mortgage rates. Start here (Feb 21st, 2022)

Best mortgage rates from top lenders

We looked at the 40 biggest mortgage lenders in the country to see how their interest rates stack up. The following list compares averages interest rates from 2020, the most recent data available at the time of writing in February 2022.

The 25 companies with the best mortgage rates on average are as follows:

| Mortgage Lender | Average 30-Year Interest Rate, 20202 |

| Freedom Mortgage | 2.92% |

| Better Mortgage | 3.03% |

| Citibank | 3.05% |

| Guild Mortgage Co. | 3.15% |

| American Financial Network | 3.16% |

| loanDepot | 3.17% |

| Guaranteed Rate | 3.17% |

| CrossCountry Mortgage | 3.17% |

| Prosperity Home Mortgage | 3.17% |

| Homepoint | 3.18% |

| New American Funding | 3.18% |

| Bank of America | 3.19% |

| Quicken Loans (Rocket Mortgage) | 3.20% |

| Supreme Lending | 3.20% |

| American Pacific | 3.21% |

| Primary Residential Mortgage | 3.21% |

| Gateway Mortgage Group | 3.22% |

| Stearns Lending | 3.23% |

| Movement Mortgage | 3.24% |

| Academy Mortgage Corp. | 3.24% |

| Caliber Home Loans | 3.25% |

| Paramount Residential Mortgage Group | 3.25% |

| Finance of America | 3.26% |

| LendUS | 3.26% |

| Citizens Bank | 3.27% |

Note that average rates shown in this table are from 2020, when rates were near record lows almost all year. Today’s mortgage rates could be higher than what’s shown.

You can still use recent interest rates as a tool to compare lenders side by side. But before you lock in a loan, you’ll want to get custom interest rates from a few different lenders to make sure you’re getting the best deal available today.

Which mortgage lender has the lowest closing costs?

Closing costs are around 2–5% of the loan amount on average. That’s over $4,000 on a $200,000 loan – a considerable amount of cash.

Just like mortgage rates, you can shop around for the lowest closing costs to minimize your out–of–pocket fees.

Here’s how the top mortgage lenders compare for total loan costs, according to 2020 data from HMDA.

| Mortgage Lender | Average Total Loan Costs, 2020(as % of Average Loan Amount) 2 | Example: Upfront Costs for$250,000 Mortgage |

| Supreme Lending | 0.64% | $1,612 |

| Citibank | 0.83% | $2,070 |

| PNC | 0.90% | $2,248 |

| Chase | 0.99% | $2,470 |

| Better Mortgage | 1.04% | $2,612 |

| Wells Fargo | 1.20% | $2,992 |

| Gateway Mortgage Group | 1.26% | $3,153 |

| Guaranteed Rate | 1.35% | $3,371 |

| Bank of America | 1.40% | $3,504 |

| Flagstar Bank | 1.41% | $3,531 |

| Prosperity Home Mortgage, LLC | 1.47% | $3,680 |

| LendUS LLC | 1.52% | $3,789 |

| Homepoint | 1.53% | $3,835 |

| loanDepot | 1.54% | $3,855 |

| Freedom Mortgage | 1.55% | $3,876 |

| Northpointe Bank | 1.56% | $3,892 |

| Finance of America | 1.56% | $3,902 |

| US Bank | 1.64% | $4,102 |

| Citizens Bank | 1.64% | $4,103 |

| Sierra Pacific Mortgage | 1.65% | $4,114 |

| American Pacific | 1.68% | $4,201 |

| Fairway Independent | 1.75% | $4,369 |

| Bay Equity LLC | 1.75% | $4,377 |

| Caliber Home Loans | 1.75% | $4,382 |

| Movement Mortgage | 1.79% | $4,481 |

When you’re shopping around, note that some closing costs cannot be negotiated because they’re set by third parties (like appraisal and credit reporting fees).

But lenders do have wiggle room when it comes to setting their own in–house fees. So if you get multiple offers, you might have some leverage to negotiate your costs down.

Some homebuyers even get the seller to cover some or all of their closing costs. But that’s not a guarantee, so you should still plan ahead for these expenses.

Compare loan offers from top lenders. Start here (Feb 21st, 2022)

What’s more important: Low mortgage rates or low closing costs?

It’s just as important to compare upfront loan costs as it is to compare mortgage rates.

Your interest rate might seem much more important because it’s with you for the life of the loan. But upfront fees can make a big difference – especially if you’ll only be in the house a few years.

Remember that most people who get a 30–year mortgage don’t keep their loan the full 30 years. In fact, homeowners keep 30–year loans for just seven years on average. And when you’re only paying interest over a short period, those upfront fees start to carry more weight compared to your interest rate.

Lenders might emphasize either low closing costs or low rates to make an offer look more attractive, while raising the other number.

In addition, lenders will sometimes emphasize one number or the other to make an offer look more attractive than it is.

For instance, lenders might advertise low– or no–fee mortgages, saying they’ll cover the upfront costs for you. But these loans typically have a higher interest rate.

Other lenders might emphasize ultra–low interest rates, but charge higher origination fees or discount points to make up for it.

So when you’re shopping for a mortgage, read your rate quotes thoroughly. Look at rates, upfront fees, and your total estimated closing costs to make sure you’re getting the best deal overall.

Find your lowest mortgage rate. Start here (Feb 21st, 2022)

How to compare mortgage rates in 5 steps

It’s easy to compare mortgage rates and fees if you know what you’re doing. There are five basic steps:

- Work on your credit rating and home-buying budget to get the best possible offer. Experiment with a mortgage calculator to see how down payment and interest rate affect the amount of home you can afford. It can be a useful warm–up exercise before you begin requesting quotes

- Figure out which type of mortgage loan you need. For example, are you in the market for a single–family home or a multi–unit property? Do you have a modest down payment, or are you rolling over sizable home equity from your current home into a new one?

- Find lenders offering the type of loan you’re looking for. First–time home buyers may be better suited for an FHA loan, while borrowers with a strong FICO score and a hefty down payment will probably qualify for a conventional mortgage. If you’re in a rural or suburban area, a USDA loan might be right for you

- Use advertised rates, recommendations, customer reviews, and expert reviews to select your best mortgage lenders

- Request Loan Estimates (“quotes”) from those lenders and compare the rates and fees in each offer

That last step – comparing Loan Estimates – is key to finding the best mortgage rate and most affordable mortgage overall.

How to read your Loan Estimates

A Loan Estimate (LE) is a standard document you’ll receive after completing a mortgage application with any lender.

The LE lists everything you need to know about a mortgage before signing on, including the interest rate, lender charges, loan length, repayment terms, and more.

By comparing multiple Loan Estimates side by side, you can tell instantly which lender is offering you the most affordable home loan.

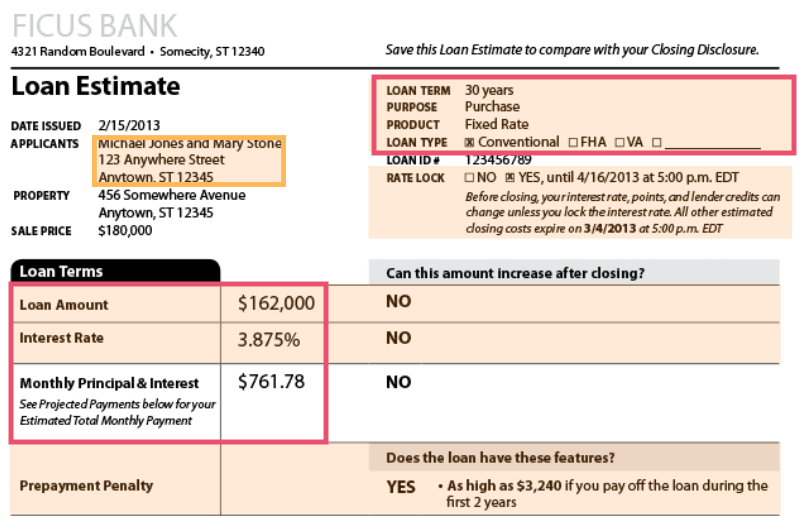

Sample loan estimate, Page 1. Image: CFPB

The first page of the Loan Estimate (shown above) clearly states your mortgage interest rate and projected monthly payment. Those are the numbers people often pay most attention to when shopping for home loans.

Your estimated monthly payment includes your loan principal, interest repayment, property taxes, and costs like homeowners insurance and mortgage insurance, if required.

But the interest rate isn’t the only part worth looking at.

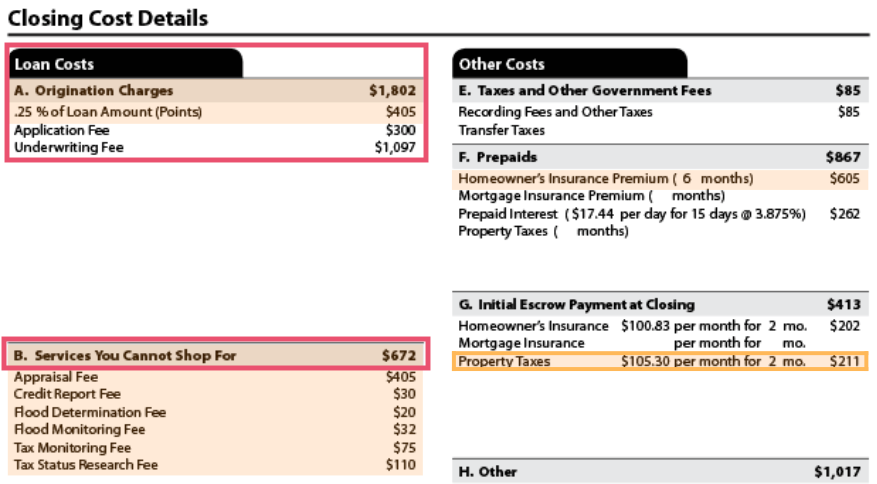

You should also compare the estimated closing costs with each lender, as well as the closing cost breakdown shown on page two.

Sample loan estimate, Page 2. Image: CFPB

Finding the best rate and fee combo

At the end of the day, the lowest–rate loan isn’t always the best offer.

Your interest rate and closing costs both have to be factored in. Their relative weight will depend on your financial goals and how long you plan to stay in the home.

For instance, if you’re only going to own the home a few years, a higher rate but lower upfront costs might make sense.

But if you plan to stay the full 30–year duration of the loan, you likely want the lowest interest rate possible. In that case, you might accept slightly higher upfront costs for a lower rate.

Find your lowest mortgage rate. Start here (Feb 21st, 2022)

Tips to get the lowest mortgage rate

If you want the lowest mortgage rate available, you have to shop around. That’s the number one rule.

But there are other strategies you can use to get lower offers from the lenders you talk to.

- Try for a last-minute credit boost. See what you can do to improve your credit before buying or refinancing. Your credit score makes a big difference in your mortgage rate, and improving it just a few points could lead to real savings

- Consider discount points. If you can afford it, you can pay more upfront for a better mortgage rate over the life of the loan. This could be smart if you plan to keep your home a long time. A discount point costs 1% of the loan amount and typically lowers your rate by 0.25%

- Negotiate your rate. Negotiating with a lender might sound intimidating, but trust us when we say it can be done. Mortgage lenders have flexibility with the rates they offer, and they want your business. A lower interest rate from a different company might be the only leverage you need to negotiate a better offer with the lender you want

- Negotiate your closing costs. Some closing costs are non–negotiable, like the third–party appraisal and credit reporting fees. But the fees your lender charges can sometimes be negotiated to save you money on the front end

- Know when to lock your rate. Mortgage rates move up and down every day. If you want to get the lowest possible rate, keep an eye on daily rate movements and be ready for a rate lock when they fall

Getting mortgage quotes might not be the most enjoyable way to spend a day. But a few hours of effort could save you thousands on your new home or mortgage refinance.

One study found that people who compare just three lenders save $300 per year on average. And if you’re a savvy shopper, you might save a lot more.

Best mortgage rates FAQ

Between 2019 and 2021, mortgage rates dropped from over 4 percent to below 2 percent. Currently, mortgage rates are hovering between 3 and 4 percent for the best borrowers. That’s incredibly low compared to the historical average of about 8 percent for a 30–year fixed–rate mortgage (based on Freddie Mac’s Primary Mortgage Marker Survey).

Historically speaking, anything below 4 percent is a very good mortgage rate. In today’s market, the best rates might be in the low–to–mid 3 percent range. Remember that the lowest mortgage rates go to borrowers with strong credit, few debts, and at least 20 percent down payment.

In our analysis of 40 top lenders, the ones with the best mortgage rates on average were Freedom Mortgage, Better Mortgage, Citibank, Guild Mortgage Company, and American Financial Network. These rankings are based on 30–year mortgage rates from 2020 (the most recent data available) Your own best mortgage rate could easily come from a different lender, which is why it’s important to compare personalized offers before choosing a lender.

If you’re only researching – and not quite ready to apply for a loan – you can use online rate comparison sites to check current mortgage rates. But if you’re ready to actually choose a lender, you’ll need to apply for rate quotes from at least 3 to 5 companies. By law, each mortgage lender must give you a Loan Estimate within 3 days of your completed application. These Loan Estimates (LEs) are in a standard format that makes it easy to compare loan terms, interest rates, closing costs, annual percentage rate (APR), and other important loan fees.

That depends. If you have a great credit score and a 20 percent down payment, a conforming loan is usually an easy choice. Home buyers in high–priced real estate markets might need a jumbo loan to afford a more expensive home price. And borrowers with an iffy credit history might prefer an FHA loan – backed by the Federal Housing Administration – which has more lenient guidelines. Other options include VA loans backed by the Department of Veterans Affairs and USDA loans backed by the U.S. Department of Agriculture. First–time home buyers should work closely with their loan officer to find the best mortgage for their financial situation.

The first step is to decide what type of mortgage loan you need. Then you can focus on lenders offering that program. Online reviews and recommendations from friends, family, or a real estate agent can also help narrow down your list. The final step is to choose 3–5 lenders you like the look of, apply for preapproval with each one, and compare their rates and lender fees to find the most affordable option.

Mortgage rates depend on a number of personal factors including your credit score, credit report, down payment, and debt–to–income ratio (DTI). The type of loan you use and the lender you choose to work with will also have a big impact on your rate. Finally, overall rate trends are determined by what’s happening in the broader U.S. economy. Current mortgage rates are low because economic uncertainty driven by the coronavirus pandemic has pushed them down over the past two years.

Typically, yes. The bigger your down payment, the lower your mortgage interest rate will be. That’s especially true with conventional loans (those not backed by the federal government). Your down payment will affect your homeownership costs in other ways, too. The less money you borrow, the lower your monthly mortgage payments will be. And if you put at least 20 percent down you can avoid private mortgage insurance (PMI), which should save you a couple hundred dollars or more on each monthly payment.

Jumbo loans – those that exceed conforming loan limits – are considered ‘non–qualified’ (non–QM) mortgages. That means their rates might be slightly higher than conforming loans. As with all types of mortgages, though, your rate depends on factors like your credit score and down payment. If your personal finances are in great shape, you could likely find a very competitive jumbo loan rate.

Most homeowners choose a fixed–rate mortgage because these loans offer safety and stability. With an FRM, you know your mortgage rate and monthly payment will never change unless you choose to refinance. Adjustable–rate mortgages often have lower interest rates at first, but these can increase after the initial fixed–rate period. And that puts homeowners at risk of having a higher – potentially unaffordable – mortgage payment later on.

That depends on your personal finances. Most homeowners prefer a 30–year mortgage because these loans offer lower monthly payments. 15–year mortgages have the benefit of lower interest rates and lower total interest payments in the long run. They also help you build home equity more quickly. However, your monthly payment amount would be much higher because you have to pay off the same loan amount in a much shorter term. Your lender or mortgage broker can help you compare loan options and find the right term for your budget.

What are current mortgage rates?

Current mortgage and refinance rates are still at historic lows, creating great deals for home buyers and homeowners.

Comparing loan offers from a variety of lenders is key to finding your best rate. But rate shopping is just one part of the home buying process.

Getting the right loan type – and saving money on closing costs and other fees – can help you lower your overall borrowing costs.

Be sure to look at fees, loan terms, and long–term borrowing costs as well as interest rates when you’re mortgage shopping. That’s the surest way to save money on your new home loan.

Show me today’s rates (Feb 21st, 2022)

1Top 40 lenders for 2020 sourced from S&P Global, HousingWire, and Scotsman Guide.

2Rate and fee data were sourced from self-reported loan data that all mortgage lenders are required to file each year under the Home Mortgage Disclosure Act. Averages include all 30-year loans reported by each lender for the previous year. Your own rate and loan costs will vary.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

[ad_2]

Source link