[ad_1]

Stay informed with free updates

Simply sign up to the Private equity myFT Digest — delivered directly to your inbox.

By now there’s a vast body of research on the performance of private equity and venture capital. In fact, there’s so much you can find a paper that will prove pretty much any point you want to make.

On the other hand, there’s been hardly any research on growth equity — a kinda halfway house between the two that was actually the fastest-growing corner of private capital until the wheels came off in 2022.

Which is why Alphaville was so intrigued by this paper, which studied a sample of over 1,500 private UK companies over 2000-2021 and looked at the difference between those that received a slug of growth equity and those that didn’t.

And lo:

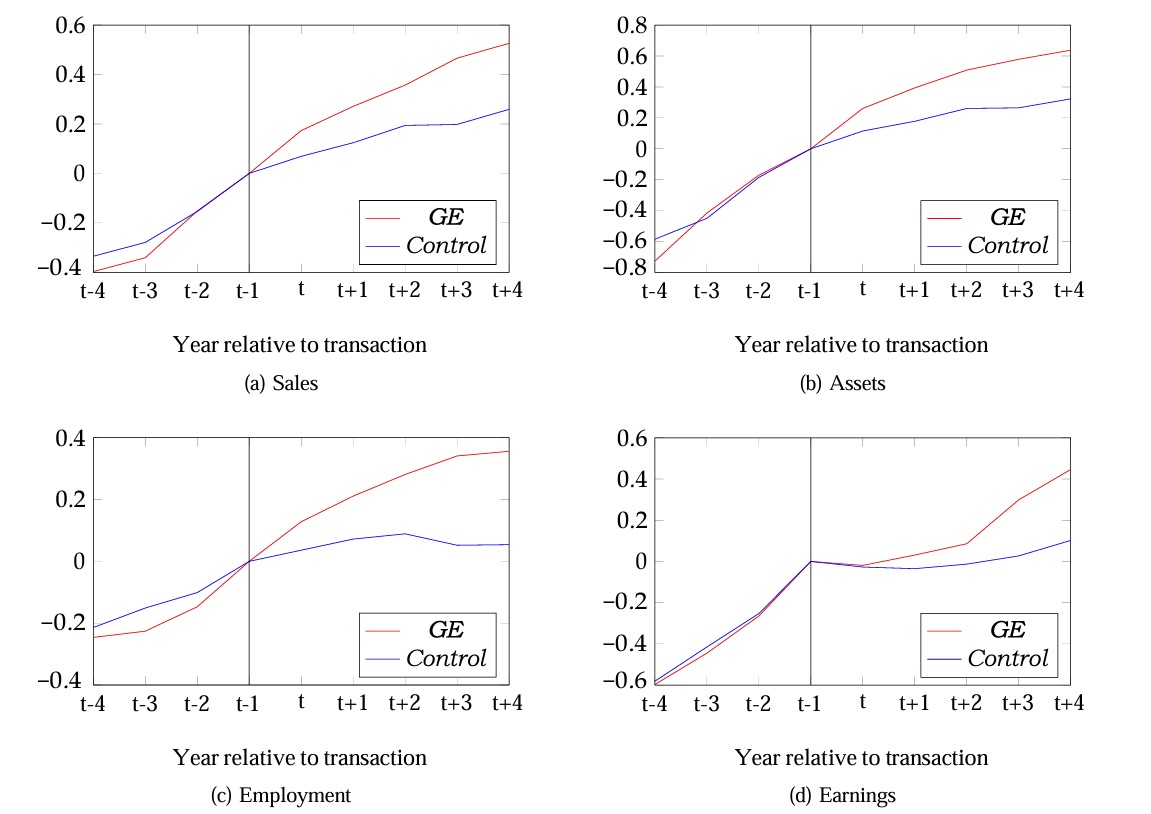

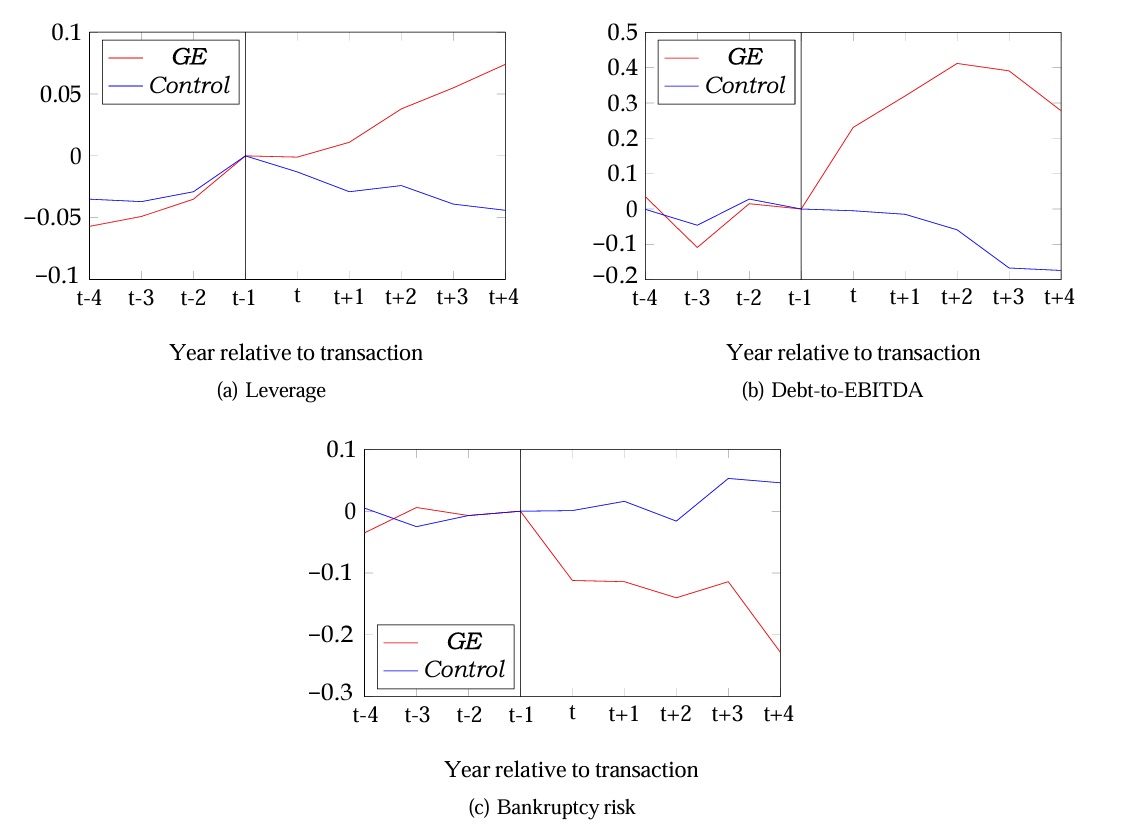

All in all, our evidence suggests that growth equity investment is a significant net positive for the UK economy . . . In a difference-in-differences setting, we document strong and robust evidence of dramatic growth in GE target firms in the post-investment period. Relative to a matched sample of non-GE- backed firms, we observe strong outperformance in GE target firms in terms of their growth in sales, assets, employment, and earnings. We do, however, unveil a darker side of GE financing. This firm growth is coupled with increased access to credit, and a substantial rise in firm leverage. Target firms’ post-investment growth in leverage greatly exceeds that of matched control firms, as does their consequent risk of financial distress. We find that treated firms can navigate distress better than their matched peers and that they are liquidated less often.

This makes intuitive sense. Companies typically raise growth equity when they are too large and well-established to be bankrolled by venture capital firms, but don’t want to sell out entirely to private equity or go public. You can think of it as very late stage venture capital, or minority mid-market private equity.

Even if they don’t get completely sucked into the private equity vortex, by even selling a minority stake they suddenly have a large financially-savvy shareholder thirsty to keep that sweet sweet growth going – before they engineer an outright sale or listing further down the road (zoomable version).

{kind=link}

And one of the main ways to do that is to borrow borrow borrow (zoomable version):

{kind=link}

And that means that growth equity-backed companies are at greater risk of bankruptcy if growth doesn’t materialise. You run with wolves, you might get bit, etc:

GE investors exit over 70% of their investments during the study period and almost 20% of exited GE-backed companies file for some form of insolvency, largely because the firms grow very fast under GE tutelage but also take on a great deal of new debt

However, the paper by Paul Lavery of the University of Glasgow and William Megginson and Alina Munteanu of the University of Oklahoma notes that troubled GE-backed companies are more likely to file for insolvency rather than outright liquidation relative to non-GE-backed companies.

Which seems fair enough. But we’d still love to know a bit more about how investors have done in growth equity — especially some of the more recent vintages.

[ad_2]

Source link