[ad_1]

Receive free Demographics and population updates

We’ll send you a myFT Daily Digest email rounding up the latest Demographics and population news every morning.

“May you live in interesting times” is not actually an old Chinese curse. But it’s awfully tempting to use it when writing about China’s economy these days.

The phrase increasingly used to describe its predicament is Japanification — a long painful stretch of real estate woes, deleveraging, economic stagnation and deflation. We wrote a chunky post about it here.

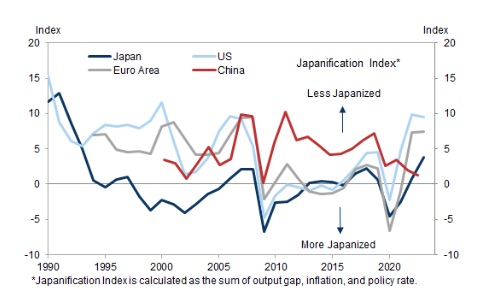

Back in 2016, professor Takatoshi Ito of Columbia University designed a simple “Japanification index” consisting of the sum of the output gap, the inflation rate and short-term interest rates In other words, the lower the score, the more Japanese you were.

Remarkably, by this measure China is now more Japanese than Japan, as this chart from Goldman Sachs shows (zoomable version):

{kind=link}

Goldman’s economists go through many of the same parallels and differences between Japan in the 1990s and China today as JPMorgan did in report we wrote up last month.

But they depart in one interesting area: demographics actually matter little to Japanification, while expectations matters a lot.

Japanification is typically viewed as an economic situation where deteriorating demographics cause structurally low growth, inflation, and interest rates. The most intuitive channel is via declines in labor input. However, despite facing this challenge, Japan’s economy still grew modestly during the last decade (except for the pandemic period), resulting in a notable decoupling of economic activity from the steadily declining working-age population . . .

. . . Japan’s experience suggests that demographics may not be as important as many think when it comes to Japanification. In China, the retirement age is 60 for male workers and 50 or 55 for female workers. Even after considering informal employment beyond official retirement age uncaptured by the official statistics, there should still be room for labor supply to expand, if needed, by increasing the retirement age. In addition, the rise of AI and its potential to replace workers may further reduce the importance of labor in driving economic growth in the future.

By contrast, the expectations channel — namely, the downward pressure of demographics on long-term growth expectations among businesses and households — was likely more important than just physical shortages of labor input in driving “Japanification” . . . When deterioration in demographics appeared likely to continue, it lowered expectations of future growth potential for the Japanese economy as a whole and thus expected lifetime income. The need to address debt overhang among corporations, as an aftermath of the bursting of asset bubble, together with the initial strong forbearance stance from both banks and the government (discussed further below), amplified this from a financial perspective. Such lowered income expectations depressed spending on consumption and investment, which in turn ushered in a negative feedback loop.

Of course, this isn’t necessarily good news for China!

It’s pretty clear that people have become a LOT more pessimistic over the past year, with slumping business investments, grim consumer confidence readings and falling economic growth forecasts.

Beijing seems determined to address this crisis of confidence by what can be termed the ostrich approach, ordering local economists to be more positive and discontinuing awkward data sets etc.

{kind=link}

Goldman argues that there might be a better way to prevent the current downturn from morphing into something nastier.

In our view, prolonged pessimism and continued downward shift in longer-term growth outlook, especially with worsening demographics and debt overhang in the background, are more threatening to China’s economic prospects than working-age population growth per se, as demonstrated by Japan’s experience. To circuit-break further deterioration in growth expectations, the government may consider emphasizing the importance of economic development, accelerating the restructuring of troubled property developers and local government financing vehicles to cut off left-tail risks, and strengthening social safety nets to encourage household consumption over the long-run.

. . . In addition to managing longer-term growth expectations, there are three other cautionary tales for Chinese policymakers. First, policy predictability and coordination are important for investment demand from the private sector, the lack of which could push the Chinese economy further along the Japanification path even in the absence of asset bubble burst. Second, financial institutions’ ability to lend needs to be protected and Japan’s experience suggests commercial banks should not be made the sole absorber of NPLs in the process of property deleveraging and local government implicit debt cleanup. Third, deflationary policies such as wage-cutting should be used with great caution as they could risk creating a wage-price downward spiral that resets inflation expectations lower and makes debt deleveraging excessively painful.

Further reading

— The great Chinese flow reversal

— China’s housing market is . . . not good

— China’s Japanification

— The implications of China’s mid-income trap

[ad_2]

Source link