[ad_1]

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. The US stock market did not blink at last week’s supposedly apocalyptic tech earnings. The S&P 500 was higher at its close yesterday than it was a week before. It seems that people want some risk exposure going into this week’s Federal Reserve meeting. There are high hopes that Jay Powell will make a noise about slowing the pace of rate increases or even pausing them. We don’t know whether that will happen or not; we wouldn’t make those noises if we were Powell, given that “sticky” prices have hardly slowed; but we are not Powell. In any case, we lay out below a case that the markets are still sleeping on the Fed’s real intentions, and the consequences of those intentions. Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

The bear case

Just as with yesterday’s bull case, we don’t necessarily endorse all of the arguments that follow. It is an attempt to lay out the best available argument for trimming risk exposure right now. Alert readers may sense that we are more sympathetic to the bears than the bulls; they will be right. But we are not banging the table (as some of the arguments below might seem to do). We just see an imperfect fit between prices and what we see as the most unlikely policy, economic, and behavioural outcomes over the next year or so. So here goes:

-

The market has priced in policy rates beginning to decline soon after they peak, and this is probably wrong. Below is a chart of evolving market expectations for the end of this year (dark blue), May (red) and the end of next year (light blue). We include May because that is when the market expects to peak. What doesn’t make loads of sense is the idea that rates will fall between then and the end of the year. Yes, a recession next year is likely (see below) and that recession will bring inflation down. But as Don Rissmiller of Strategas has pointed out, the Fed will not want to risk committing the mistakes of the late 1970s and early 1980s, when rates were brought down too soon, inflation jumped again, and rates had to be put back up. We could end next year with rates still at their peaks.

-

Valuations, though they have fallen, just aren’t that cheap. The S&P 500’s price/earnings ratio tells the story here. We are not anywhere near the lows of previous major drawdowns, such as 2001 and 2008. Lots of people think we need not approach those lows, because the recession, if there is one, will be mild. But that’s not a good bet (see below).

Others will look at the chart of cyclically adjusted P/E ratio (that is, the S&P 500 price divided into 10-year average earnings) and point out that it is bang at its average since 1995 (28). But part of the reason Cape valuations have been high since the late 1990s is because inflation has been very low and rates have been falling. That’s all over now. Stocks are not cheap.

![Line chart of S&P 500 trailing price-earnings ratio showing If you think this is cheap, better have a good reason]()

-

That valuation point goes for corporate bonds too, by the way. Spreads are higher than they were, but don’t price in much bad news. Here are BBB spreads, which are right at their long-term average:

-

There is going to be a proper recession. The 10-year/3-month yield curve recently inverted (see chart below). In the past this has predicted recession all but infallibly. It makes sense that it should do so. Such an inversion indicates that short rates (which determine so many other prices in the economy, from bank loans to mortgages) have been pushed very quickly to a level above long rates. Long rates are a very rough approximation of a neutral interest rate for the economy. If short rates are higher than long, short rates are restrictive; money costs so much it slows growth. The economy’s parking brake has been yanked. A recession follows.

An argument is frequently made that this recession will be mild because consumer and corporate balance sheets are particularly strong right now. While balance sheet strength might reduce the chances of the types of financial contagion that personal bankruptcies and corporate defaults cause, remember that monetary policy brings down spending by reducing demand. Fed tightening will cause household and corporate spending, and therefore the economy, to fall significantly. That is what it is designed to do, because that is what brings inflation down. A shallow or “technical” recession could only result from perfectly calibrated policy that the Fed has often failed to achieve in the past.

-

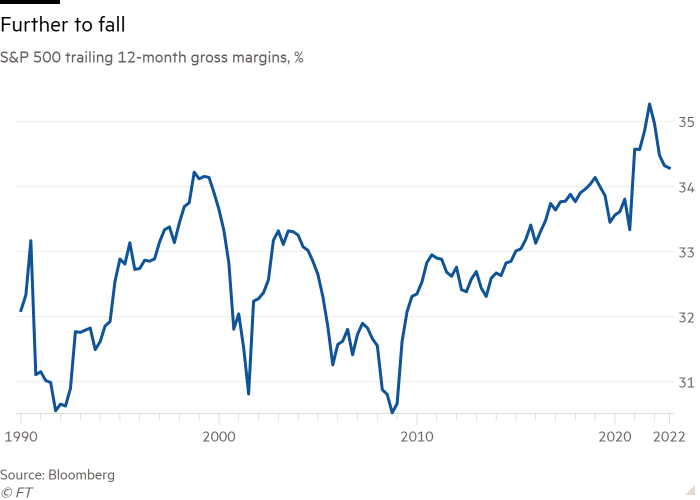

Margins have only started to compress. The coronavirus pandemic-era combination of rising input costs, shortages and high demand were a blessing for margins. Mark-ups surged as consumers spent without restraint and companies flexed their pricing power. But falling demand and an inventory bulge are now weighing on margins. And as Morgan Stanley’s Mike Wilson points out, today’s inflation is particularly menacing for margins, with producers’ input inflation falling more slowly than consumers’ price inflation. Margins, and earnings, are going to get worse.

-

Tina is toast. It used to be that you had to buy stocks because the risk-free alternative, Treasuries, yielded nothing; hence “There Is No Alternative”. That, too, is all over now. Even though falling stock prices have pushed up their earnings yield, the yield differential between stocks and bonds is shrinking.

![Line chart of S&P 500 earnings yield less 10-year Treasury yield, % showing Tina, turning over]()

-

Sentiment may have capitulated, but flows have not. Bulls make a big to-do about poor investor sentiment. It is poor, and that’s a contrary indicator. The idea is that we are near capitulation, that point where all the bad news is inscribed in the price and the only way to go is up. But the poor sentiment has not, crucially, been accompanied by net withdrawals from equity funds, which makes it seem as if capitulation remains some way off. Below are net flows into US equity funds on a three-month rolling average basis. They have only just touched zero as the extraordinary rush of money during the pandemic has subsided.

-

Illiquid markets make for violent selling. The sell-off in stocks has been remarkably orderly so far, and we’ve seen no sudden surge in the Vix. But as liquidity has dried up, other markets, like sovereign bonds or currencies, have not looked so benign. Commonly used indices for bond-market volatility (Move) and FX volatility (Cvix) are at decade-plus highs. Historically, FX volatility drives bond market volatility, which in turn creates tumult in equities, notes Michael Howell of CrossBorder Capital. Put another way, the groundwork has been laid for panicky selling should any further shocks to equities, such as earnings deterioration, occur.

If we’ve missed any brutally obvious points, on the bear or bull side, do let us know. (Armstrong & Wu)

One good read

Japan can, and should, defend the yen.

[ad_2]

Source link