[ad_1]

As tens of millions of baby boomers enter retirement, many believe they should allocate a preponderance of their life savings in instruments where income is fixed (aka bonds or fixed income). The convention “own your age in bonds” was financially justifiable when it was developed decades ago, however, the joint life expectancy of retiring couples today is far more than it was. Further, in the fixed income world today, there are two significant challenges: one secular (10 years or longer), the other cyclical. On the secular front, yields have been in a broad decline for 40 years. The U.S. 10-year Treasury yield peaked at 15.8% in September 1981 and has been in a steady decline ever since (today around 1.4%). The cyclical challenge currently is that real yields are negative. The real yield is simply the current risk- free rate minus the rate of inflation.

Mashing increased life expectancy along with secular and cyclical factors together, the result is a cocktail that is undeniably destructive to wealth and will put the comfortable retirement of many at risk. That should be somewhat intuitive if you define money correctly. The only sane definition of money is purchasing power – not currency. Today with inflation on the rise, real yields negative and little prospect for returns beyond that, bond investors are lighting their purchasing power on fire.

Most of the prospective clients that walk into our offices share two common goals:

- Live a comfortable and worry-free retirement.

- Pass as much as possible to charity and family.

Those prospects, by in large, are woefully under allocated to diversified equities for a myriad of reasons. They anchor to the convention that when one retires, they should allocate to bonds because they are “safe”. They are frozen by the bombardment of spewing sewage promulgated by the financial media designed to keep their eyes glued to advertisers. They are convinced that equities can’t go higher and questioning whether the historic record can be used to inform decisions ahead. In other words, they use the four most dangerous words in investing: “this time is different” (credit to legendary investor Sir John Templeton).

The goal of this commentary will be to demonstrate that from a relative perspective, given the two goals above, the primary risk to a retiring couple today is an arbitrary allocation to fixed assets. However, if your thesis is “this time is different”, it’s important to address the fundamental reason why an efficient market rewards a risk premium to equity investors.

Equities offer a premium return over bonds. Period. According to data published by Robert Shiller, the average real (net of inflation) rolling 10-year excess return of stocks over bonds going back to 1871 is 4.33%, and the average since 1946 is 4.88%. However, the historical equity risk premium over bonds is not true because over history it has been true. Without a premium return in equity investments, the greatest economy in the world would not exist as we know it.

We all have had friends approach us to invest in their next great start-up “idea”. They come to us because no bank lends to an idea. It lends to mature businesses with assets and cash flow – by definition those businesses carry less risk. Start-up businesses can only raise money via equity (or debt that converts to equity) because 90% of them fail. By that very nature, the premium return on equity investment comes from the risk of investing in something that is far less certain. Amazon could never have started without a world that rewards a premium return for equity investment. What about Apple? Or Tesla? Find a company that has changed the world starting as a transformational idea with borrowed money. We don’t know of one. Nothing that the Federal Reserve, politicians, and/or (insert the talking point of the day) does changes that fundamental truth.

That distinction in equity investments extends to mature companies as well. If you buy a bond from Amazon, you stand ahead of equity holders in the capital structure. You have certainty in your interest payment and reasonable security in the return of your principal. While the price of the bond may fluctuate based on movements of interest rates, with a financially sound company your dollar loaned is worth a dollar at maturity. However, as a loaner you do not participate as Amazon changes the world. The owner participates in that progress even as her dollar fluctuates in price around the news of the day. Equity ownership is riskier than bond ownership, and hence the equity is expected to pay a premium over the debt.

Our job as advisors is to help clients formulate a plan that drives the most critical decision in the pursuit of optimal real-life investment returns: the relationship between equity and fixed assets. Most advisors take the easy path – they pander to a client’s emotional proclivity for “safe” by constructing expensive portfolios of bond funds that are packaged with more risk than commonly understood. The industry at large doubles down and designs complex products that create the illusion you can have your cake (something that is safe) and eat it too (with higher returns). If you are ever curious what financial alchemy in the retail space that looks like, read Morningstar’s damning white paper on one of the worst examples – “Structured Notes: Buyer Beware” (if you want a copy, let us know, we will send it to you).

As established prior, the premium return on equity investment is a natural law of our world. However, it’s important to understand how it applies to portfolio decision making. While the investment community forecasts expected returns in various asset classes, the numbers themselves are not as critical applying relative advantage of owning versus loaning to portfolio decisions.

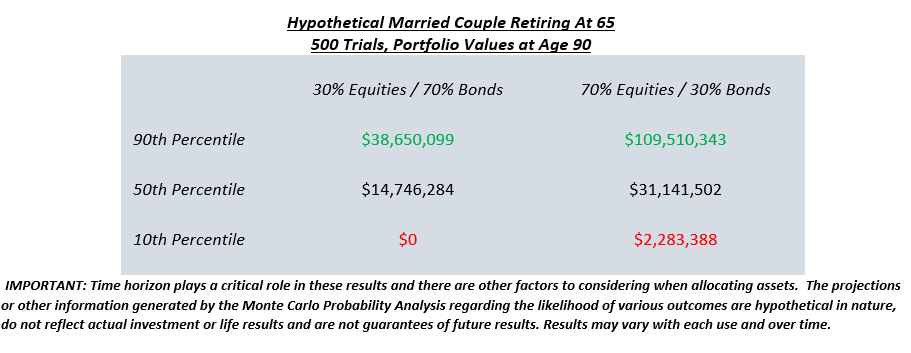

We can use Monte Carlo simulations to help understand that relative advantage. In these simulations, the worst outcomes start with highly negative consecutive equity returns in the beginning of retirement. In examining the best and worst case for a retiring couple using varying asset mixes, the results comparing 500 different return paths are compelling, and for most clients unexpected.

One would expect that in a multi-decade retirement plan with a world of worst-case equity returns that a higher allocation bonds would produce better outcomes. When looking at the results of hypothetical portfolio outcomes at life expectancy, in all findings the 10th percentile (50th worst) result vacillates remarkably close in a portfolio of 30% equities when compared to a portfolio of 70% equities. However, the 90th percentile (50th best) is magnitudes better in the latter. From that perspective, isn’t it appropriate to redefine the conventional understanding of portfolio risk?

We are not advocating for portfolios without bonds. All clients should have fixed assets in a planning framework to help weather inevitable bear market periods – that reserve helps equities in realizing their full potential. However, the asymmetry in worst/best outcomes in our Monte Carlo testing of retirement portfolios supports our assertion that an arbitrary allocation to fixed assets impacted by inflation is the primary risks to a multi-decade retirement and legacy investment portfolio. Most everything else is just noise.

E. Peter Tiboris is a 20-year industry veteran and the President of Strongpoint Wealth Advisors.

Christopher Bremer is director of research and advisory at Strongpoint Wealth Advisors,

[ad_2]

Source link